DISCLAIMER: Car-accident and insurance laws vary by state — including how uninsured/underinsured motorist coverage works, whether you can "stack" policies, and what you can collect from an at-fault driver personally. This article is general information only, not legal advice. Talk to a qualified attorney in your state as soon as possible about your specific wreck.

Hey folks, Tall Chuck here.

If you're reading this, odds are you're staring at one of these situations:

- An uninsured driver wrecked your car.

- The other driver only had minimum limits, and your medical bills are already way past that.

- An insurance adjuster just said, "Sorry, that's the policy limit — that's all there is."

From my 7-foot-tall view, I see this more than I'd like: good people get crushed financially because someone else chose to drive with little or no insurance at all.

Let's talk about what you're really up against, how UM/UIM coverage works, and how to build a case when there just isn't enough coverage to make you whole.

The Big Picture: Two Scenarios, One Big Problem

Car crash involving an uninsured driver

Car crash involving an uninsured driver

Scenario 1 — Uninsured Driver: The at-fault driver has zero insurance. They may be driving on a suspended license, they may have let their policy lapse, or they may have never had coverage at all. If you have UM coverage, you make a claim with your own insurer. If you don't have UM, you can sue — but if they have no assets, a judgment is worth about as much as a used napkin.

Scenario 2 — Underinsured Driver: The at-fault driver has insurance, but their policy limits are so low they don't come close to covering your actual damages. Example: they carry $30,000, your injuries are worth $150,000. You collect their $30K, then turn to your own UIM policy for the rest.

In both cases, you're left with a gap between what you need and what the at-fault driver can pay. That's where UM/UIM coverage comes in.

UM vs. UIM Coverage: What's the Difference?

| Uninsured Motorist (UM) | Underinsured Motorist (UIM) | |

|---|---|---|

| When it kicks in | At-fault driver has NO insurance (or hit-and-run in many states) | At-fault driver's limits are TOO LOW to cover your damages |

| Who pays | Your own insurer, under your UM policy | Your own insurer, under your UIM policy (after at-fault policy is exhausted) |

| What it covers | Medical bills, lost wages, pain and suffering (varies by state/policy) | The gap between the at-fault driver's limits and your actual damages |

| Required in Texas? | Must be offered; you can waive in writing | Must be offered; you can waive in writing |

| Key risk if you don't have it | You're stuck chasing assets from someone who likely has none | You absorb the difference out of pocket |

Think of UM as: "If the other driver didn't carry insurance, my own policy becomes their insurance — up to my UM limit." Think of UIM as: "If the other driver's insurance isn't enough, my policy covers the gap."

What Are Policy Limits and Can You Stack Them?

Policy limits are the maximum an insurance company is obligated to pay under that policy. If the at-fault driver has a $30,000 policy and your case is worth $300,000, the insurer can pay $30,000 and say, "We're done." That's legal.

Stacking means you can sometimes combine more than one UM/UIM policy or more than one vehicle's coverage to increase the total available money. For example, if your car and your spouse's car each carry $50,000 in UM/UIM, a stacking state might let you access up to $100,000. Whether stacking is allowed — and how it works — is very state-specific. That's one of those "you really need a lawyer who knows your state" situations.

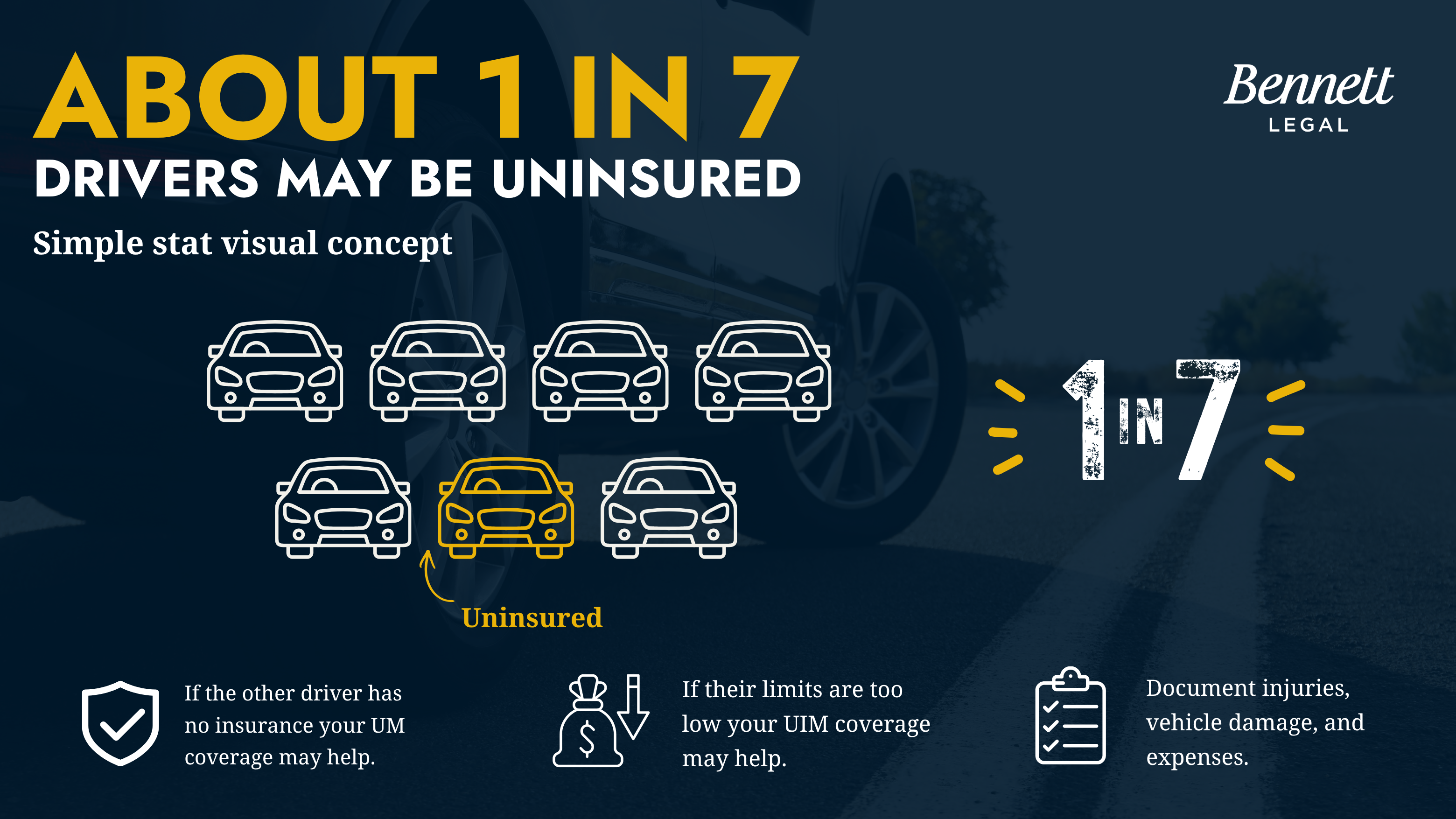

What Happens If the At-Fault Driver Has No Insurance?

About 1 in 7 drivers may be uninsured

About 1 in 7 drivers may be uninsured

If you have UM coverage, you make a claim with your own insurer. They step into the shoes of the at-fault driver's insurance, but you still have to prove fault and damages — and your insurer will fight you on value just like the other side would.

If you don't have UM coverage and the at-fault driver has no insurance and no assets, the hard truth is: no insurance + no personal assets = very little to collect, no matter how strong your case is. This is why UM/UIM is some of the most important coverage you can carry. It protects you from somebody else's bad choices.

Tall Chuck says: "I tell every client the same thing: UM/UIM isn't optional. It's the coverage that has your back when somebody else's bad choices leave you holding the bag. Check your policy today."

Can You Sue an Uninsured Driver After a Car Wreck?

You absolutely can. But the real question is: will you actually collect?

If the driver has no house, no real assets, low income, and debts — you may spend time and money chasing money that isn't there. Sometimes you can garnish wages or lien property, but if they're truly judgment-proof, you end up with a moral victory instead of a financial one.

Suing an uninsured driver is less about "Can I?" and more about "Is there any realistic way to get paid if I do?" A lawyer can help you look at the driver's background, other possible coverage sources, and whether a lawsuit is a smart move or just extra stress.

How Do You Build a Case When Coverage Is Thin?

Step 1: Treat It Like a Normal Injury Case — Because It Is

Get medical care, follow doctor's orders, document symptoms, time off work, and daily limitations. Preserve evidence: photos, witness info, police report. Build the strongest possible case on fault and damages regardless of who's paying.

Step 2: Identify All Possible Insurance Policies

This is where having a lawyer with a tall view matters. Look beyond the obvious: your UM/UIM, policies covering you as a resident relative, passenger coverage from another vehicle, umbrella policies, and employer or commercial policies if the other driver was on the job. You'd be surprised how often there's more than one policy in play.

Step 3: Exhaust the At-Fault Driver's Policy First

In many states, before your UIM kicks in, you must settle with the at-fault driver's insurer and — this is critical — get your own insurer's permission before you sign that release, so you don't accidentally waive your UIM rights.

Step 4: Prepare for a Fight With Your Own Insurer

Once you file a UM/UIM claim, your insurer puts on a different hat. They're the one paying the next dollar. Expect them to question your treatment, argue your injuries were "pre-existing," and push low settlement offers. A well-documented case and a lawyer make a big difference here.

For more on how adjusters operate — even your own — check out: 6 Tactics Insurance Adjusters Use After a Car Wreck

Tall Chuck says: "If an adjuster says, 'That's all we can pay — the policy limit,' do not just take their word for it. Ask for proof of the policy limits in writing, and talk to a lawyer before signing any release. Once you sign away your rights, it can be near impossible to go back and tap other coverage you didn't know about."

Dealing with an uninsured or underinsured driver and not sure what coverage you have? You don't have to figure this out alone. Bennett Legal can review your full coverage picture for free. Get your free case review — bennettlegal.com/contact

What You Should Do Right Now

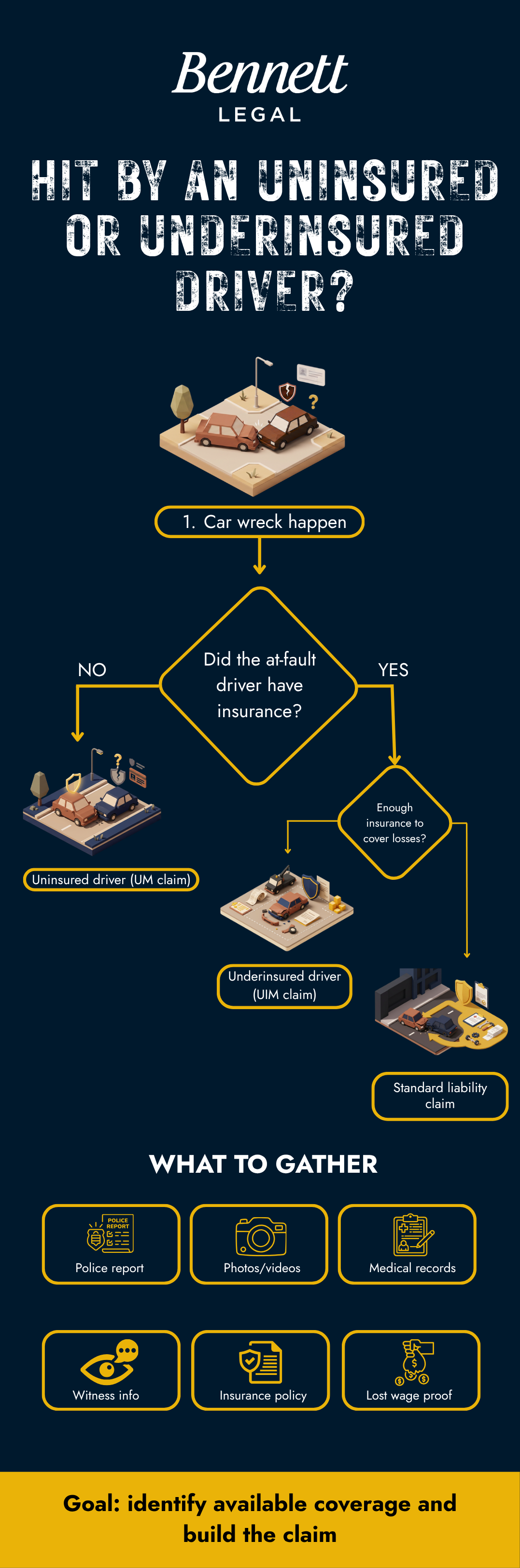

What to do if you get hit by an uninsured or underinsured driver

What to do if you get hit by an uninsured or underinsured driver

Whether the uninsured driver wrecked your car or the at-fault driver just has tiny limits, here's your action list:

- Get medical treatment and follow up. Your health comes first. Gaps in treatment will also be used against you later.

- Get a copy of the police report. This helps show fault and may list insurance info (or the lack of it).

- Gather your policies. Your auto policy, any policies where you might be a listed driver or household member, and any umbrella policies. Look specifically for UM/UIM coverage.

- Do NOT rush into a low settlement. If an adjuster waves a small check at you fast, it might be because they know your claim is worth more — but only if you don't sign it away.

- Ask a lawyer to review the full coverage picture. There might be another vehicle's UM/UIM, a resident-relative policy, a work-related policy, or stacking options you don't know about.

For the full step-by-step on what to do after any car wreck, see our complete guide: From Crash Scene to Courtroom: A Car Wreck Lawyer's 6-Phase Roadmap

Tall Chuck says: "If you're renewing or shopping for car insurance, don't skimp on UM/UIM just to save a few bucks. The driver who hits you doesn't care how responsible you are. UM/UIM is the coverage that has your back when they don't."

How Bennett Legal and Tall Chuck Can Help

Stand Tall and Call Bennett Legal

Stand Tall and Call Bennett Legal

When someone calls and says "The driver who hit me has no insurance and the adjuster says that's all the money there is" — here's what we do:

- Map out every possible source of coverage. We dig into the at-fault driver's policy, your UM/UIM, possible stacking or multi-policy options, and any employer or commercial coverage. We don't just take an adjuster's word for it.

- Build the strongest case on fault and damages. Medical records, lost income, future losses, expert testimony when needed. Even with low limits, a strong case maximizes settlement offers.

- Give you straight talk about reality. Where the money might come from, where it likely won't, and what your realistic range of recovery looks like. No sugar-coating. No scare tactics.

- Handle the stress so you can focus on healing. We deal with the adjusters, watch the deadlines, and protect you from signing away your rights too early.

Reach out to Bennett Legal for a free case evaluation or call (972) 972-4969

Tell us what happened, what insurance you know about so far, and what the adjusters are telling you. We'll help you understand your UM/UIM options, see whether any policies can be stacked, and decide whether it makes sense to sue the at-fault driver personally.

You don't have to untangle this mess by yourself. You focus on your health and your family. Let me and my team focus on the insurance and the fight.

Keep standing tall, folks. Chuck's got your back.

Free consultation

Dealing with an uninsured driver?

Get the legal help you need. Free consultation with a Dallas car accident attorney.